Aug 4, 2020|

JD Big Data Panorama: Chinese Brand Consumption Soars under COVID-19

by Ella Kidron

The 2020 Chinese Brand Development Report released by JD Big Data Research Institute and the Communication University of China (CUC) and other research organizations, as well as media groups such as Outlook Weekly, China Comment, and Credit100.com, looks at the key growth drivers and trends emerging in the consumption of domestic Chinese goods. The report, which is based on JD’s data, explores not only how domestic brands have performed, but also how social e-commerce and the consumption of services continues to drive reliance on domestic brands.

It is no secret that international brands are a bright spot for JD.com. As a platform that emphasizes high quality and authenticity, imported brands are well-loved by the e-commerce giant’s over 380 million consumers, as was demonstrated during this year’s 618 Grand Promotion.

While international brands remain a huge growth driver, domestic brands, which have proven their worth and reliability under the pressure of COVID-19, continue to gain the trust of JD’s high quality consumption base across China.

80% of brands on JD realizing over RMB 100 million yuan in H1 are Chinese brands

According to the data, in the first half of 2020, 80% of the brands on JD realizing over RMB 100 million yuan in sales were Chinese brands. Chinese brands also accounted for nearly 90% of brands whose sales have increased by more than 50%. On the whole, the improvement and growth rate of Chinese brands is clear.

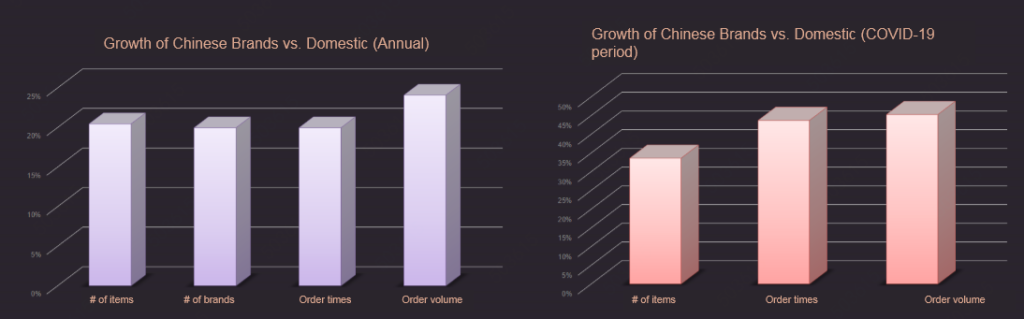

Growth of Chinese brands faster than that of imported brands

In 2019, the year-on-year growth rate of the number of Chinese brand goods, the number of orders placed and the order volume was more than 20% higher than that of imported brands. Under the influence of COVID-19, in the first quarter of 2020, this number reached more than 30%. Looking at the growth rate of the transaction volume of Chinese brands vs. imported brands, the growth rate of the proportion of Chinese brands in categories such as maternal and child, sports, and personal care has been high. This demonstrates that consumption of Chinese brands in categories where trust is of particular importance continues to rise.

Chinese brands gain more consumers’ trust under COVID-19

In terms of the particular characteristics of consumption of domestic brands under COVID-19, the data reveals that for the first quarter of 2020, transaction volume of Chinese computers and office supplies grew 109% YOY, among which computers grew 194%. Chinese brand computer and office category notebooks, printers and other supplies accounted for the large increase in proportion as compared with 2019, among which the transaction volume growth of notebooks exceeded 30%.

Domestic fresh food products played an essential role in ensuring supply in the pandemic, transitioning from a complementary to comprehensive role. In the first quarter of 2020, transaction volume of domestic fresh food increased by 156% compared with the same period last year, among which transaction volume of meat (pork, beef and mutton), vegetables, poultry and eggs increased by 655%, 183% and 166% respectively YOY. Compared with the first quarter of 2019, domestic fresh food categories with the highest increases included pork, beef and mutton, prepared dishes, and instant food, among which the growth of transaction volume of pork, beef and mutton exceeded 20%, outpacing fresh produce and seafood, and leaping to the top of the fresh category.

Chinese brand health and protection products have also seen a rise. In the first quarter of 2020, transaction volume of domestic masks increased 10 times year-on-year, while transaction volume of homecare, masks and blood glucose meters increased significantly compared with the first quarter of 2019, becoming the top three health-related categories. The increase makes sense given the limited mobility of people during COVID-19 and the inconvenience of hospital visits, leading them to rely more on homecare and remote assistance.

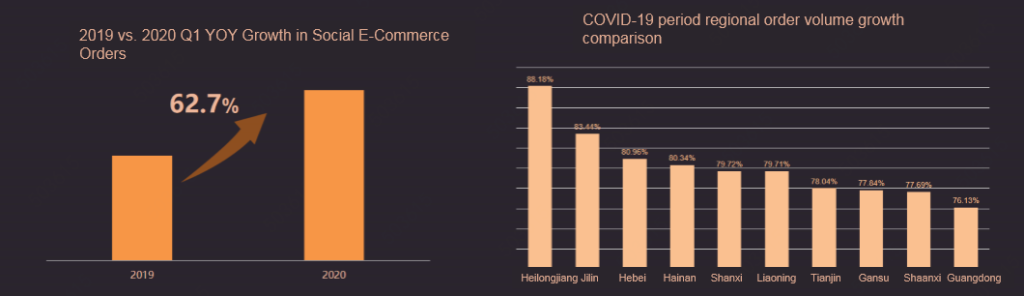

The “acquaintance effect” in social shopping channels

The public health emergency of COVID-19 has brought new opportunities for development thanks to social e-commerce. The “acquaintance effect”, high popularity of daily necessities are among the main characteristics of social channel consumption. The data shows that, affected by the epidemic, consumers have increased their dependence on trusted relationships among acquaintances, thus directly promoting social e-commerce consumption based on personal relationships. Social e-commerce orders increased by more than 60% in the first quarter of 2020 compared with the same period last year. At the same time, the number of social e-commerce orders from the northern regions of the country, which are more sensitive to the acquaintance effect, increased significantly compared with the same period last year.

Social channels provide users with “more approachable consumption”, boosting the consumption potential of low- and medium-priced goods. Under the influence of COVID-19, small- and medium-sized domestic brands rely on cost-to-performance advantages to expand their user bases, and the new user effect for these brands is demonstrably higher than that of their imported brand counterparts. Compared with the same period in previous years, orders of fresh food, household cleaning and paper products, kitchen utensils and other products increased significantly. In terms of user group portraits, social e-commerce participaiton of village and town residents, enterprise employees and other groups is relatively high, thanks to the emphasis of these groups on performance-to-price ratio as well as the strong interpersonal relationships in the social environment. Social e-commerce is based on emotional trust, and this sense of trust can be very effective for brand building.

Online consumption of domestic goods expands from “things” to “services”

The increasing maturation of online-to-offline (O2O) models is leading to the rapid growth of the scale of service-oriented consumption of Chinese brands. According to the report, in 2019, the overall scale of service-oriented consumption of domestic brands more than tripled, compared with the same period the previous year, satisfying consumers’ diversified service needs. Among services, the auto-aftermarket is setting the pace, with vehicle maintenance and repair, ETC (the leading automated toll payment provider in China), car decor, washing and other services in consumers’ good graces. Renovation and installation services have become a highlight of online consumption. As consumers pay more attention to home quality, interior decoration has increased significantly, as high as 20-50 times. In addition, during the COVID-19 period, overall sales of “agency services” increased fivefold compared with the same period in 2019. There is a clear indication that online services will continue to prosper and become a new driving force for economic growth.

Lower-tier city penetration remains key focus

Lower-tier city penetration remains the most important growth point for domestic goods. According to the report, from 2019 to the first quarter of 2020, e-commerce channels continued to help Chinese brands penetrate the lower-tier markets. In the 5th and 6th tier cities, Chinese brands accounted for a higher proportion of consumption. Transaction volume of Chinese brands in the lower-tier markets also increased more than that of the same period last year. Domestic brand consumption in the first-tier markets is also strong, indicating that more users with high consumption power have significantly increased their awareness and trust of domestic products.

Jun 19, 2026|

JD.com 618 Grand Promotion Sets New Record for Shoppers Alongside Rapid Growth in Service Consumption

Beijing, June 19, 2026 —JD.com’s 618 Grand Promotion concluded with a new record in the number of users placing orders this year, alongside rapid growth across a wide range of consumer services.

As China’s largest brand-led e-commerce platform, JD.com continued to serve as an important growth platform for both established brands and emerging businesses. As of 11:59 p.m. on June 18, the number of major brand new product launches increased by more than 500% year on year during this year’s 618. The number of new small and medium-sized merchants participating in the promotion rose by more than 62%, , while over 3,000 merchants participating in 618 for the first time surpassed RMB 1 million in transaction volume

Consumer demand for services grew strongly. Transaction volume for JD Home Services’ home cleaning services increased by more than 200% year on year, while transaction volume for home appliance cleaning services rose by over 300%. Orders for JD Health’s in-home nursing and care services for people with limited mobility increased more than 400%. Orders for home appliances and home living products supported by JD.com’s integrated delivery and installation services increased by more than 120% year on year. Orders for the delivery and installation of electric vehicle charging stations rose by 80%, while orders for doorstep repair services for two-wheelers, including electric bicycles and motorcycles, increased 800%.

Strong growth was recorded across key product categories. Transaction volume for AI-powered consumer electronics increased by 100% year on year, while more than 1,800 home appliance and home living brands achieved growth of over 100%. Premium smartphones and slim-and-lightweight laptops recorded year-on-year growth of 300% and 100%, respectively.

JD Super, the supermarket division, recorded double-digit growth in both transaction volume and user numbers, with more than 1,000 brands achieving year-on-year transaction volume growth of over 100%. More than 2,000 fashion brands, including UNIQLO, doubled their transaction volume, while 2,100 small and medium-sized fashion merchants recorded growth of more than 200%. At JD Fresh, more than 1,500 brands saw completed order volumes increase by over 100% year on year.

Livestreaming also played a pivotal role in connecting consumers with products and brands. During 618, the total amount of time users spent watching e-commerce livestreams increased by more than 100% year on year.

Omnichannel Growth Expands Consumer Touchpoints

JD.com continues to innovate and expand its offline retail formats, creating more connections between brands and consumers, while providing additional touchpoints to meet evolving shopping needs.

JD MALL recorded a 22% year-on-year increase in overall footfall and a 32% increase in order volume. With the opening of its first stores in Shanghai and Hong Kong, the number of JD MALL locations has exceeded 30. JD MALL’s Shanghai Qibao store, which officially opened on June 12, welcomed more than 156,000 visitors and generated over RMB 120 million in sales during its first three days.

Meanwhile, more than 5,800 JD.com’s various electronics stores recorded year-on-year order growth of over 100%, while footfall more than tripled. Among them, more than 3,000 stores achieved transaction volume growth of over 100%.

Across other offline formats, JD Outlet stores recorded a 110% year-on-year increase in transaction volume. Visits to JD Pharmacy’s self-operated stores increased nearly fivefold, while the value of completed parental health check-ups at JD Health’s examination centres nearly tripled. Orders at JD Aesthetic Medicine’s self-operated offline clinics doubled month on month. Across more than 4,000 JD Auto Service stores and over 40,000 third-party partner locations, the total number of vehicles serviced increased by more than 50% year on year.

In Hong Kong, the number of Kai Bo Supermarket stores surpassed 100, with sales during 618 increasing by 52% year on year.

International Business Gains Strong Growth

JD.com’s cross-border import business, JINGDONG Cross-border, saw the number of products sold increase by 60% year on year. Transaction volume for Royal Salute, children’s oral care brand Jordan and Chloé increased by more than 200%, while Google, Rolex and maternal and baby care brand Masata each recorded more than fourfold growth.

On June 15, Joybuy, JD.com’s European online retail business, launched its Summer Black Friday promotion, delivering strong first-day sales. Both the number of users placing orders and total order volume reached new highs, while more than 800 brands more than doubled their transaction volume compared with Joybuy’s launch day in March.

During this year’s 618, JD.com also became China’s first online departure tax refund store for international visitors. The service allows travellers to browse and purchase a wide range of tax-refundable products through JD.com’s app, providing a more convenient and efficient digital shopping experience while visiting China.

Meanwhile, both user numbers and transaction volume on JD Global Sales more than doubled year on year. The platform introduced direct shipping for large home appliances and furniture to Singapore, Malaysia, Vietnam and Thailand, together with shipping incentives. Sales in the relevant categories increased by more than sixfold year on year.

AI-Powered 618 Brings Intelligence Across Industries and Everyday Life

This year marked the first JD.com 618 in which AI was integrated across the company’s full range of business scenarios and industries. Building on JD.com’s distinctive business model and supply chain capabilities, its AI applications now span more than 3,000 scenarios across retail, logistics, healthcare, industrial services, food delivery and home services, bringing AI from a wide range of industries into consumers’ everyday lives.

Nearly 100 new smart hardware products powered by JoyInside, an AI agent for smart hardware, were launched during 618, while the number of newly connected devices more than tripled year on year. JD.com’s private-label J.ZAO AI toys also delivered strong performance, with sales increasing by more than 150% month on month.

AI-powered products emerged as a major consumer trend. Transaction volume for products including AI glasses, AI PCs, large-screen AI smartphones and AI learning devices increased by 100% year on year, while AI mini workstations and AI sensing devices recorded growth of more than twentyfold.

Transaction volume for newly launched smart home appliances and home living products also increased 2,000% year on year. Transaction volume for AI-powered electric toothbrushes and smart cups increased by 300%, while AI washing machines, connected refrigerators, smart coffee machines and AI mattresses each recorded month-on-month growth of over 100%.

Demand for robotics also accelerated. Sales volumes of humanoid robots increased more than tenfold year on year, while sales of exoskeleton robots increased more than sixfold.

AI Tools Support Merchant Growth and Operational Efficiency

JoyStreamer, JD.com’s digital avatar livestreaming solution, recorded significant growth during 618. The average number of merchants using the solution to livestream each day increased 500% year on year, while cumulative GMV generated through JoyStreamer increased by 100%. Order conversion rates rose by 77%.

JD.com’s Oxygen Vision design agent supported the large-scale creation of AI-generated images, written content and videos, helping merchants improve their overall operational efficiency by more than tenfold.

JoyMarketing combines precise consumer insights, intelligent strategies and human-like interaction to help merchants better match consumer needs with relevant marketing content. Total interactions through JoyMarketing exceeded 800 million during the promotion. JD.com’s intelligent customer service solution has served more than one million merchants.

During the promotion, JINGDONG Logistics’ LangzuTech automated warehousing solution processed 34 million orders. Autonomous delivery vehicles transported a cumulative 5.53 million parcels.

*Unless otherwise specified, data reflects the period from 8:00 p.m. on May 30 to 11:59 p.m. on June 18, 2026.

Jun 12, 2026|

JINGDONG Cross-Border Welcomes South Korea’s 11Street to Launch Official Flagship Store on JD.com

JINGDONG Cross-Border (JD Cross-Border), the import e-commerce platform of JD.com, welcomed South Korean e-commerce leader 11Street, an affiliate of SK Group, as it officially launched its flagship store on JD.com. This partnership marks a major milestone for JD.com’s “10 Billion Giga-Growth Plan,” aiming to bring premium Korean goods directly to Chinese shoppers while helping Korean brands enter the Chinese market more effectively.

Starting June 11, customers can easily find the store by searching “11Street Overseas Official Flagship Store” on the JD.com app. The grand opening will feature store-wide discounts, free shipping on orders over 159 RMB (approximately USD $23), and exclusive member benefits. The store will offer a wide array of premium products, ranging from popular K-Beauty brands and health supplements from top curators like Olive Young to home goods and trending lifestyle products popularized by Korean pop culture.

The partnership, which began in February, leverages JD.com’s advanced supply chain and logistics network to provide a one-stop solution for Korean merchants. JD.com provides comprehensive support from business registration and compliance to marketing and shipping, effectively removing traditional hurdles for international brands.

“Cross-border trade between China and South Korea has evolved into a total ecosystem partnership,” said a representative from JD Cross-Border. “Our approach combines direct procurement and a robust marketplace with advanced logistics advantages, offering emerging and premium Korean products a trustworthy gateway to the Chinese market.”

11Street noted, “Partnering with JD Cross-Border allows us to bridge the gap between Korean retailers and Chinese consumers, ensuring that our brands can grow efficiently while maintaining the high quality and service our customers expect.”

By introducing top-tier Korean cosmetics, food, and baby products, the arrival of 11Street reinforces JD.com’s position as the go-to destination for high-quality global goods. This initiative further advances JD.com’s “10 Billion Giga-Growth Plan” launched in 2025, which aims to introduce 1,000 new international brands to China over three years and reach an absolute sales target of RMB 10 billion (USD $1.4 billion), significantly expanding the variety of imported goods accessible to Chinese families.

(vivian.yang@jd.com)

Dr. Shen: Positive Consumption Growth is Important for China’s Economy in H2 2020

Dr. Shen: Positive Consumption Growth is Important for China’s Economy in H2 2020